During 2018, there have been many events that moved the Indian markets towards life time highs followed by often getting corrected. We are at the end of year and markets have witnessed a correction of 8% after reaching its life time high in August 2018. I have been thinking if at these current levels, are Indian markets over-valued or can we still expect it to reach new highs in coming year? Before writing down my thoughts on 2019, today I discuss about the current levels.

I have done a very primary evaluation of valuation of markets, using P/E Ratio of market index, GDP growth, 10 year G-Sec yield and comparing their movement over a span of 13 years. (I have extended the normal period of 10 years by 2-3 years, as 2008 has been an exception and I wanted to showcase market trends before 2008).

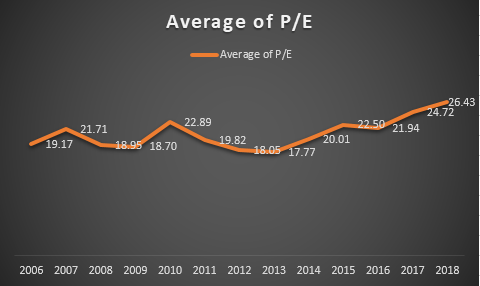

As per the below chart, the current P/E Ratio is 26.43 times, whereas the mean for 13 year period (2006- 2018) is 20.53 times. The ratio has peaked in last 2 years from 21 times in 2016 to 26.43 times in 2018, which states the market expectations on India’s performance have increased, but the corporate earnings haven’t increased to the desirable levels.

When we look at the trend of P/E ratio, in 2008, the ratio dropped from 21.71 to 18.95 times, a correction of 12.6%. Post 2008, the ratio averaged at 19.9 times till 2015.

Just before 2008, the gap between the GDP growth and P/E ratio widened. On the break of sub-prime crisis, there was a steep fall in both GDP and P/E ratio. Post 2008, both moved in tandem, As markets and valuation are guided by growth in the economy. In 2015, GDP peaked at 8.15%, followed by slower growth in 2017 at 6.62%. However, for 2018, the growth had increased and for year 2019, is further expected to increase as per the estimates.

But, as we observe the trend, currently, the gap between the GDP and P/E had widened again.

Bond yields are often an indicator of economic cycles and they tend to rise when the growth slows down and are peaked during recessionary period, as the market commands higher risk premium. Whenever the bond yields increase, markets have also undergone correction. In the below chart, as we see the bond yields decreased from 8.53% in 2014 to 6.72 % in 2017, but in 2018, yields have risen to 8%. This is also impacted by the rise in the interest rates by RBI and other impending factors.

Thus, considering these few key determinants, is current market valuation, justified enough. Are the current levels sustainable? According to me, they aren’t and Indian markets might witness a correction. To add, yesterday’s tumble of US markets on Christmas Eve and future events may bring rippling impact on India as well.

There is a lot to watch for in 2019. Few of them at global level are US markets tech fallout, Italian sovereign default, china slowdown and debt problems, emerging nations slowdown coupled with currency depreciation and rising debt, Brexit effects, Japanese Bear market, highly volatile oil markets. For India of course, as we approach the Parliament election season, corporate performances, banking sector performance-NPAs-MSME sector lending-farm loan waiver and impact of global events.

Benjamin Graham quoted in chapter 8 of The Intelligent Investor – ‘The longer a bull market lasts, the more severely investors will be afflicted with amnesia; after five years ago or so, many people no longer believe that bear markets are ever possible. All those who forget are doomed to be reminded; and, in the stock market, recovered emotions are always unpleasant.’

Thank you for reading. Kindly share your thoughts in below comment box, you may further share it, if you liked it. I will be coming up with my thoughts on markets in 2019. Merry Christmas !!!!

Glossary:

Market Index - Nifty 50

Bond Yield - 10 year Indian G-sec

Source:

tradingeconomics.com, RBI Statistics, NSE database

Comments