Mark Twain once stated – History does not repeat, but it rhymes. Economies, markets, businesses operate in cycles. These cycles originate from the very nature of human behaviour and psychology, led by supply and demand, greed and fear, thus driving the business activities. Short term cycles occurring over period of 8-10 years repeat and several of these transpire into long term cycles that occur over century, once in lifetime of an individual. An archetypical cycle is formed by various occurrences having cause and effect relationship. Every event in a cycle has an effect, causing the next series of events, thus building the cause-effect relationship. An archetypical cycle of rise and fall denotes that the economic booms are followed by busts, market bulls are followed by bears, however the busts and bears may not end at where they started but may end higher, thus also signifying the rising trajectory of a long-term economic cycle.

Exhibit 1 denotes the rising growth trajectory of India’s GDP since 1961. The economic cycle of India has been growing, despite economic booms and busts. These short-term cycles are impacted by either indigenous or exogenous variables, causing the markets to fall and rise.

Many investors are concerned about year-to-year economic growth, be it high, low, negative or positive, which are short term considerations. Although they are important for making investment decisions, their importance fades as long-term considerations become more relevant. Most of the cycles that attract investor’s attention consist of oscillations around a central tendency. While the oscillations matter over the short run, over the long run the underlying trend holds more importance (1).

The short-term cycles fuelled by gravity (the pull backs) and momentum (the bull rides) occurring repeatedly may seem different, the theme and mechanisms remain same. The study of long-term cycles composed of short-term cycles also depict the cause-effect relationship of the wealth and power of the nations, the rise and fall of empires. These long-term cycles appear occur over several decades, a century and once in a lifetime of an individual. The variables of an archetypical economic cycle include the macro environment, global situation and an economy’s sensitivity to it, corporate growth, debt situation, fiscal policies, investor psychology. Further study of these variables helps us understand and gain a futuristic view of where we stand, which part of cycle we are in and what lies ahead.

Last two years have been ferociously volatile for economies and markets. The world is witnessing once in 100 years pandemic, once in 75 years invasion in Europe, burgeoning inflation in 40 years and all time high debt levels in major developed economies of the world. Today, the global economy is gripped by rising price levels, disrupted supply chain, restricted availability of energy, climate catastrophes, increasing geo-political tensions and feared recessionary slump.

Just before the pandemic set in, United States was at the end of its interest rate hike cycle as part of its quantitative tightening programme and rates had already begun sobering down (Exhibit 2)

The former quantitative tightening succeeded the generous quantitative easing programme post Great Financial Crisis (GFC) of 2008 to boost the economic activity. As the US economy was severely hit during the GFC, to boost the economy US resorted to ‘Quantitative Easing (QE)’, in other words ‘printing of money’.

Quantitative Easing is a mechanism through which liquidity is infused in the market through purchase of securities in target markets like Treasury bonds, mortgage bonds and other financial securities. In a typical QE, the newly printed money gets added onto the liability side of the balance sheet of the central bank and securities bought on the asset side.

Management of liquidity is key to economic activity. The economic growth is driven by the amount of money circulating in the economy. When the money in circulation is excessive, central banks reduce the liquidity in economy through various tools. One of key tool used by central banks to manage money supply is Interest rates. Interest rates are increased as part of monetary policy tightening and lowered as part of expansionary policy. When the economy dries up and requires boosters to larger extent, interest rates are lowered as much as possible till it reaches zero. When zero interest rates are not enough to drive the economy, central banks have no option but resort to printing of new money, as part of stimulus programmes. The question here is whether new money created is with backing of any real assets?

Now we take a step back and understand the currency system that the world currently operates in. Money is a medium of exchange and store hold of wealth that can appreciate with time. That is where the concept of time value of money is conceived. When we say money is a medium of exchange that means it can be exchanged for something in return - goods and services, that is productive in nature. Hard money currency system (metal coins) restricts the supply of money to the extent of precious metals’ supply. Centuries back, precious metals were used as medium of exchange. With advancements in financial and banking systems, paper backed currencies grew in circulation. The paper money were basically claims on hard money. Money and credit supply can be easily created in this system, which may cause run on the banks when the claims on hard money increase more than the supply of hard money. After the Great Depression of 1929, US for first time gave up on the gold currency system in 1933 and adopted the Fiat currency system, where the supply of money is not backed by any real assets. Fiat money is a government issued currency, which it can capriciously print at any time at its whim and fancy. In 20th century, many countries officially gave up on gold standard and adopted the Fiat currency system. US officially delinked Dollar value to Gold in 1971. Intrinsic Value of any currency is derived from its underlying assets, thus in Fiat currency system, if the supply of money exceeds the productivity in an economy, the currency loses its value. This can be understood in terms of Real economy and Financial economy. Real economy consists of the production or supply and demand of goods and services. Financial economy involves supply and demand of money and credit. When the real economy faces supply constraints or high demand, pushing the prices higher, financial economy kicks in where, by using monetary tools the supply of money is reduced in the economy to bring down the demand and reduce inflation. Similarly, when the demand for goods and services is weak and economic activity needs a boost, the supply of money is encouraged and increased by use of expansionary monetary policies like reduction in interest rates and printing money when the interest rates touch rock bottom. When we look at the past cycles, every economic boom or bust is followed by monetary and fiscal policies resulting into the next series of swing in the cycle. Thus, the bulls are followed by bears and bears are followed by bulls. When the bulls are over extended, it creates a bubble and when bears are over-extended it leads to crash. The human tendency of over doing leads to bubbles and crashes.

The euphoric feeling of – ‘Tonight I am gonna party like its 1999, and the best will stay forever’ leads to over extended bullish positions in the market without consideration to the fundamentals. This is what happened before the Dot Com bubble of 2000. The market frenzy for internet and technology stocks had heightened which finally led to the crash. Nasdaq that had reached 5048 in March 2000 at its peak then crashed to 3321 in April 2000, bottoming to 1114 in October 2002. Peter Theil in his book Zero to One quoted – ‘The era of cornucopian hope was relabelled as an era of crazy greed and declared to be definitely over’. This precedes the melancholy of worst is here to stay forever. As the dust settled and the sentiments improved, focus of markets moved from clicks to bricks and the next boom was seen in the housing market, which led to 2008 financial crisis and housing market crash. Every crash is followed by a recessionary period, then the central banks kick in with their guns to bring down interest rates and amass the markets with freshly printed money. The bipolarity of Mr. Market causes the oscillating swings and ups and downs of the cycles, that provides opportunities to those informed well about the cycles and how to position themselves well to make a fortune. In coming paragraphs, we will have a look over these series of repeating economic policies and its impact on the financial securities in the context of recent events.

Pre-Pandemic Situation

Just before the pandemic set in, US interest rates were already reducing due to underlying risk of economic slowdown and uncertainty due to trade war between US and China. As the pandemic spread in early 2020 amid rising fears of economic loss, central banks looked over reducing the interest rates. US Federal Reserve slashed down the interest rates in March 2020 by 50 bps to 1%. Generally, interest rate cut have a positive impact on equity markets as the lower interest rates pushes up the valuations. But, US equity markets reacted negatively by shedding 2.94% in a day perceiving the potential risk to the economy. US Bond markets (one of world’s largest bond markets) also responded accordingly. The bond yields bottomed out to lifetime lows of 0.9% (Exhibit 3).

As markets perceive US treasuries as safe haven, the rush for US Bonds ramped up the bond prices, thus dropping the yields (As bond prices increases, yields fall and vice versa). Like falling knives, S&P 500 lost 1129 (33%) points from 3383 in February 2020 to 2254 in March 2020 and Indian markets lost 4745 points (38%) from 12254 to 7509 during the period. Due to lockdown across the globe, the economic activity came to a standstill. The industries & transport were closed, unemployment rose, and demand shrunk. Reviving the economy was need of the hour and in response, the global central banks launched their favourite piece of stimulus packages through Quantitative Easing. The interest rates were already at rock bottom levels in March 2020. Thus, US did not have much room for further decrease in rates. US infused around $ 4 trillion of fresh liquidity and the balance sheet size grew from 4 trillion $ to 8.8 trillion from 2020 to 2022. The already ballooned balance sheet post 2008 GFC is now inflated around 9- 10 times since then (Exhibit 4).

European Central Bank also resorted to Quantitative Easing to deal with the Sovereign Debt Crisis in 2011-12 caused by Greece’s default and inability to meet its debt obligations, which brought it to the brink of default. Since then, ECB’s balance sheet size has enlarged 4-5 times (Exhibit 5).

Since balance sheet management has become a widely used key tool by central banks as shock absorber against crisis, it is important to deliberate whether these measures adopted are sustainable for the long-term stability of the economy. As already discussed about QE, any accumulation of assets equals increase in the corresponding liabilities for the central bank. Purchase of securities by central bank from the market and infusing liquidity in return, raises the prices of those assets and lowers the yields in short run. This affects the credit spreads, for example, when the Fed responded to the Covid 19 crisis through QE measures, the credit spreads that had increased significantly quickly reverted to pre-crisis levels (2). (Credit Spreads are difference between the yields of corporate bond and interest of risk-free asset.) The long-term interest rates consequently reduce. Thus, increase in liquidity over short run may have impact on medium term price stability. Moreover, fall in short term rates and increase in long term rates shall be deterrent for asset prices over long run, due to inflationary risk of excess liquidity.

Pandemic Policies

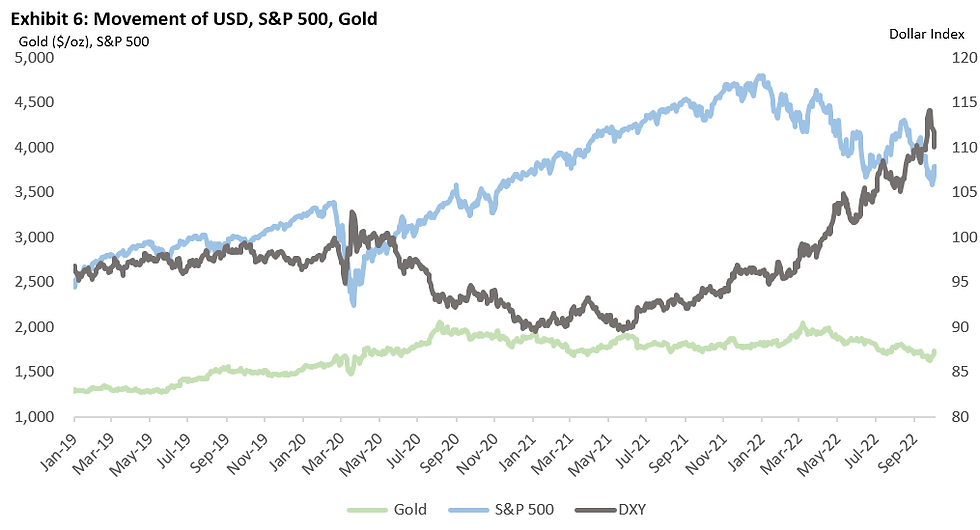

During the year 2020, as US central bank flooded the markets with liquidity, the asset prices increased. The bond yields remained lower and bond prices higher. The stock markets rejoiced on the policy decision and rebounded to touch new highs. The law of demand & supply applies to assets, commodities, currencies. Gold, popularly known as crisis hedge, touched new highs of $2000/oz. Central banks, global investors resort to Gold as the hedge and this buying spree had led gold to break many resistances. US Dollar, perceived as another safe-haven asset class plunged in value as its supply increased and interest rates decreased. Thus, it can be inferred that printing of money leads of devaluation of currency. (Exhibit 6)

As for India’s story, the Reserve Bank of India reduced the interest rates to as low of 3.25% in March 2020 and increased to 4% in May 2020. These levels were all time lows for India and was cautiously reduced to boost the economy, considering India’s high inflationary history (Exhibit 7).

Despite lockdown restrictions and continued covid outbreak, the rally in equity markets was unprecedented across the globe. The infusion of liquidity by central banks drove equities higher. The decreasing interest rates brought down the discounting factor and pushed up the multiples. Higher multiples led to higher valuation of equities, with minimum congruence with the prevailing fundamentals. Inflow of foreign capital in Indian equity markets continued and these accelerated the price rise. Nifty skyrocketed from 7533 in March 2020 to 15371 in February 2021 and 18420 in October 2021. FIIs (Foreign Institutional Investors) poured in INR 2 lakh crores in cash segment alone, fuelling the equities ride. Another key element was the participation of retail segment in the equity markets. The demat accounts more than doubled from 40.9 million to 100 million. As the economy recovered in 2021, global GDP increased by 5.8% in 2021 and India grew at 8.9% as against -6.6% in 2020. US registered annual GDP of 5.7% as against GDP of -3.4% in 2020 (3).

It is amusing to see how economies and markets transpired into different cycles from time to time. As they gradually transition from stage to another, lot of enthusiasm and uncertainty grows. In 2020, we pondered over how will our lives emerge during the pandemic; we had a range of speculations of our own kind. Pandemic changed our lives in many ways, and it has resulted into newer emerging trends. Economic policies and geo-political situations have played a vital role in how the present has transformed. While the expansionary policies like stimulus packages, lower interest rates received tremendous applauds from the stock, bond, commodity markets, today we concerningly glare at the raging inflation that is impacting our lives and those globally at a larger scale.

Transpiring into Inflation Cycle

The formula for inflation is simple. Create more demand or reduce supply. The gushing liquidity infused by central banks has caused the circulation of money in the economy at a frenetic pace. This resulted in people having more money to spend. When they have more money to spend, the demand for the goods and services rises. When such money is not used for increase in productivity, rather diverted to asset classes, the gap between the real economy and financial economy widens and the prices of assets rises, even causing asset bubbles. The ubiquitous concern of inflation is what we are grappling with in the present moment.

Blame it to the on-going war conditions between Russia and Ukraine alone and disrupted supply chain, but if we look over conditions in 2021, some inflationary signals were already flaring. The widely used commodity, crude oil having a bearing on our daily lives, had begun rising over multi year highs. Exhibit 8 shows that commodity prices had begun their multi-year ride in February 2021.

As there is a direct relationship between inflation and commodities, an uptick in commodities can provides a reasonable view of inflation. While then, the central banks chose to foresee it as mere ‘transitory’. US Federal Reserve balance sheet has ballooned multi-times and similar trend was observed in European nations as well. In June 2021, the Fed begun giving signals of possible tapering down of the balance sheet, in other words, reducing the liquidity in the markets through asset sale programme and reducing its balance sheet size. Regardless of the signs and their taper tantrum, the balance sheet tapering did not happen at required scale and the inflationary situation got exacerbated. They initially misjudged the inflation being mere transitory and believed it was a temporary effect of supply shocks and pent-up demand and that prices would settle down. However, prices continued to rise. In year 2022, global economic situation morphed into a tumultuous smorgasbord of events leading towards its nemesis. There are multitudes of challenges in front of the global leaders and central banks to prevent a painful meltdown, avoidance of which appears farsighted.

Geo-political Stratagems between Russia, Europe & US

Amidst burgeoning inflation, few may have envisaged the geo-political stress to worsen causing widespread impact on oil and gas prices and making many nations energy deficit. With the commencement of Russia's attacks on Ukraine in February ‘22, many other countries, especially the West began imposing package of sanctions in areas of trade, transport, petroleum, banking and capital markets with the aim of crippling the Russian economy. Russia is second largest producer of crude oil and gas and largest exporter of natural gas to the world. Thus, dependencies on Russia for energy is evidently severe.

In March, US ordered a ban on imports of crude oil, gas and coal from Russia to the US. In April, UK pledges to end dependency on Russian coal and oil and end gas imports as soon as possible. In response to the military aggression against Ukraine, EU has imposed slew of sanctions on Russia in areas of trade, transport, banking etc. EU introduced measures prohibiting import of coal, crude oil and petroleum products from Russia into the EU. Since the dependency of EU and UK economy on Russian gas is large, it is not possible to flip off the switch so quickly. As a result of the ban, Russian crude oil imports into EU and UK fell, but EU still remains biggest market for Russian crude, according to IEA (International Energy Agency). UK has already stopped importing Russian crude and EU will ban imports from December to strip Russia from revenue for war.

Imports from the United States have replaced about half the 800,000 barrels of lost Russian imports. The United States could soon overtake Russia as the main crude supplier to the EU and the UK combined. Interesting point here is that US does not import any gas from Russia. US’ dependency on Russia for natural gas and crude oil is negligible. As Russia restricted supplies to Europe, it causes the global gas prices to rise. High oil and natural gas prices have increased the cash flows of most U.S. shale gas producers, leaving many of these companies with hefty amounts of cash. Source: S&P Global.

In response to the sanctions, Russia retaliated by stopping the natural gas supplies to Europe through the crucial Nord stream pipeline, that connects Russia to Germany and supplies natural gas to majority of Europe. Europe relies on Russia’s natural gas supplies for 40% of its energy requirement. Natural gas is used for generation of power & electricity, heating purposes, transport, cooking fuel. As a result, gas prices in Europe have soared more than double since Ukraine’s invasion.

Consumers and corporations are hard hit by the price rise. Electricity bills have already tripled. Major industries have begun furloughing workers and cutting back expenses due to high electricity bills. This has made situation of Europe utterly dire and have forced them to reopen previously renounced coal plants and nuclear sites. Due to high temperatures during this summer, the energy consumption touched peak owing to large use of air conditioning. With the hot temperatures, severe droughts crippled hydro & nuclear power generation. Shifting for electricity from natural gas to coal has driven up the coal prices.

70% of European fertilizer companies rely on ammonia extracted from natural gas. Thus, operations of these companies have also halted. This has led to increase in the cost of fertilizers which further translates into increase in food prices. Even operations of core manufacturing companies like that of steel and glass also are at risk.

Since the disruptions into its energy systems, Europe has been scrambling to re-align its supply chain and energy sources. While reducing reliance on cheaper Russian gas, it must look onto other sources like Qatar, United States and others. Long term changes in supply sources would require increase in production by hubs, laying down pipelines (pipeline is the cheapest mode of transport) and storage terminals, which generally can happen over a period of 2-5 years. Even though Europe wants to re-align its supplies, it can happen over a period. Over the short term, there are limited countries that can shore up supplies in the short term. Investment in natural gas infrastructure is expensive. Demand is expected to increase as cold winters approach. Thus, the European economy is on a double-edged sword. As the supply side is not expected to get resolved in short run, the only way to address the situation is to reduce demand through rationing. However, in winters it will be difficult to reduce the demand for heating purposes. Europe stands most affected and vulnerable from the aftermath of sanctions. It can be collectively inferred that reducing demand and rationing is only way for Europe to cope with the energy crisis.

Over last few weeks, natural gas prices have somewhat cooled down, as the inventories have increased owing to stock piling for winters. Gas storage sites continue to fill as countries switch from gas to coal in power plants and industry and increase imports of LNG. Storages are generally filled during summers and are expected to get empty as winter sets in. They are brimming at 80% of their capacity and target to each 95% of capacity by November. Mild or harsh winters will further guide the natural gas consumption of the continent. As of now, paying more than double prices for energy, Europe still stands at the risk of manufacturing shutdown with uptick in the demand across the globe. This may have devastating impact of unemployment, high inflation, low economic activity, with likely public unrest and divisions.

Another variable in governing the oil and gas market is the production by OPEC (Organisation for Petroleum Exporting Countries). OPEC is a cartel of several oil producing nations which decides the supplies and thus prices of crude oil in the global market. OPEC has a major share of oil production and supplies around the globe. Amidst the oil and gas crisis, OPEC declared production cut of 2 million barrels per day in October 2022, which may drive crude oil prices higher.

Walking down the memory lane, decade of 1970s recorded hyper inflationary situation and is popularly known for Energy crisis and Stagflation. The world then faced two oil shocks in a decade, rattling the economies. First oil shock was caused due to embargo imposed by OPEC against US and second was triggered due to Iranian revolution reducing the oil output.

Grim Economic Situation

Inflation in United States, United Kingdom, Europe is at multi decades high (Exhibit 9), with core inflation remaining stubborn. In August 2022, US registered inflation of 8.3%, UK -9.9%, India – 7%. In September, Euro zone inflation reached record high of 10%, up from 9.1% in August 2022.

We discussed in former paragraphs, how interest rates are a key tool to manage the liquidity in an economy. Interest rates are decreased to boost a depressed economy and increased to cool down a heated economy. When the interest rates are increased, the flow of money and credit in the economy reduces, thus impacting the cost of credit and demand for goods and services. If interest rates are increased aggressively, the production & demand sentiment gets impacted causing the nation to enter a recessionary period.

To combat inflation, central banks have begun to hike interest rates. US Federal Reserve (The Fed) has aggressively increased 75bps for 3 times in a row, raising interest rates from 0.25% in March 2022 to 3- 3.25% in September 2022. The Fed has vowed to bring down inflation and indicated a painful experience ahead. Technically, when an economy records two consecutive quarters of negative GDP, it is into a recession. US registered GDP of -0.6% and -1.6% in last two quarters. Severity of rate hikes is based on the impact on the economic activity and prevailing leverage on the economy. The global markets have remained cautious on the central banks’ interest rate decisions. Till date, interest rates are at below levels: -

· US Inflation: 8.30%; Interest rates: 3-3.25 %

· Eurozone Inflation: 10%, Interest rates: 1.25%

· UK Inflation: 9.9%, Interest rates: 2.25%

· India Inflation: 7%, Interest rates: 5.9%

This tool resorted by central banks are blunt and work only on the demand side. Interest rate management cannot address the supply side concerns, especially when the supply chains across the world are disrupted. Higher interest rates supress the sentiments of households and business, causing a painful slowdown. In order to bring down inflation, generally government can increase taxes to reduce the disposal income in hands and curb consumption, increase labour supply, lower energy costs, reduction of import duties etc. However, these policies take time and time is of the essence here. In face of the fast pace of inflation and current geo-political situation, central banks have adopted the tool – Interest Rate Hikes. The underlying point that remains is that the large fiscal stimulus packages released in the market to achieve superficial growth by central banks causes the economy to overheat. And to cool down an overheated economy, one takes harsher steps, which further impacts the economy hard. This is what is happening now when decade long stimulus packages and zero interest rates left the world economy unable to sustain higher interest rates and shrinking liquidity.

This had also caused the Great Depression of 1929. Post World War I, US gained from the trades as a result of the new world order. The new world order had period of peace and prosperity fuelled by great innovation and productivity and capital markets boom. These produced huge debts and big wealth gaps. In the Roaring 20s, a lot of debt (promises to deliver paper money against limited supply of gold) was created to buy speculative assets, especially stocks. To curtail that, Federal Reserve tightened the monetary policy in 1929, which caused the bubble to burst and resulted into beginning of Great Depression. The Great Depression brought economic pain to many nations and increasing wealth gaps and fighting over wealth within and between nations, leading to wars which began a decade later (4). Post turmoil, it took 25 years for Dow Jones to recover and return to pre-depression levels. 1970s inflation was targeted by Fed by increasing the interest rates starting from 1978 increasing to as high as 20% in 1980, much above the level of inflation, after which reduced the rates slowly. The rates hikes brought worst global economic pain since the Great Depression. Markets continued to decline and countries that borrowed in US denominations defaulted due to sky-rocket rates.

Increase in the interest rates leads to rise in debt service and economies on the edge with borrowings in the currency that increases rates become perilous and on verge of defaults. If we look at the debt situation of US itself, the debt-to-gdp ratio is 137% (2021 statistics), whereas in 1980s, it was 30%. Thus, then US had room to increase the rates as its debt was not as high as today. Today, every 100 bps increase in rates shall increase the debt service burden of US by 1.37%. Nations that hold debt in its own currency, can devalue debt by devaluation of currency and printing more money. However, nations that hold debt in foreign currencies are at the perils of high interest rates. Thus, the countries that hold US-denominated debt are at risk of increase in debt service burden and economic sufferings, more so when they are import reliant.

Another factor that is causing turmoil in the global currency markets is the rapid appreciation of US Dollar. As the interest rates rise, the capital that once moved out of US in low interest rate regime, returns to safe haven currency. US Dollar still retains its peak position in the currency market and is perceived as safe-haven currency (irrespective of its own problems) and rates hikes have caused the US Dollar to accelerate. This has caused a sharp dive in global currencies. While USD has gained, many countries are facing sharp depreciation of their domestic currency against USD (Exhibit 10). The fragile economic conditions of Euro zone and UK due to energy crisis and inflation, coupled with USD gain had led to sharp depreciation in Euro and British Pound. Amidst the global turmoil, India remains resilient and has not seen wreaking impact of currency depreciation.

The impact of interest rates and risk feared by the markets can be observed from the turmoil in equity markets and bond markets. US Nasdaq lost 21% from its all-time high in Dec-21 and bond yields have surged from 1.3% to 3.7% following the rate hikes. US is at the cusp of slowdown and potential recession; it is also much feared to bring along a deep recession across the globe and withering of economic health of high debt laden nations. US has indicated to hike the rates from current 3-3.25% range to 4.5% upto December 2022. Other central banks have joined too. Uncertainty due to rate hikes prevail across the globe. Lately, UN called on the central banks to halt the interest rates increases fearing global economic downturn. The risk due to high debt, fear of economic slowdown, may cause the rate hikes to cool down in coming months. In contrast, continuance of rate hikes will continue to rattle markets.

If we have learnt anything from history, is that wars are expensive and have wiped out many nations. Many economies that funded wars are out of power to support their economies, nor can they print more money as that may risk their currency’s value. World War I and World War II have set enough examples for us to learn from mistakes and not to recur it. But those who do not remember the past, are condemned to repeat it. When something is popular to over extremity, expect it not to last for long and for trend to change to opposite direction soon.

The factors that we have discussed in this note causes the upswings and the downswings in the economies and capital markets. On top of it, the geopolitical crisis has fuelled the situation making it more challenging for global leaders to cope with the crisis. History has not seen many cases when the economic crisis, natural disaster and revolution / war has occurred at the same time, thus, making our current times difficult to predict and devise policy measures to stay in the curve and ahead of the curve. The odds are it is much likely that the global factors, changing geo-political arc, weakening health of developed nations, brings us to possibility of changing world order, shift in the long-term cycle and rise of new empires. The path towards a new rise shall be painful but it once it is over; invites creation and innovation, long periods of peace and prosperity and reigning long term productivity and growth.

- Ushma Zunzavadiya

Note 1: This article was originally published in the December 2022 edition of LLIM Journal of Research ISSN 2249-4740 and the author acknowledges the permission from the journal for publishing it on this platform.

Note 2: Data, Charts and references are upto 06th October 2022.

References:

(1) Mastering the market cycles by Howard Marks p.48 – oscillations around the short-term cycles will cancel out in the long run but changes in the long run will make the biggest difference in our long-term experience.

(2)https://www.stlouisfed.org/on-the-economy/2021/february/credit-spreads-financial-crisis-covid19

(3) World bank database - https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG

(4) Principles for Changing World Order - p 337 by Ray Dalio. 3 big forces causing major cycles that are – Long term Debt and Capital Markets Cycles, Internal Order and Disorder Cycle, External Order and Disorder Cycle.

Comments